The window to amend prior year returns for the R&D tax credit is closing in 2026.

The July 6, 2026, deadline is not just a date on a calendar—it’s the day the IRS stops allowing you to fix 2022-2024 tax mistakes.

This is not new information. What’s surprising is how many companies still haven’t acted on it.

The One Big Beautiful Bill Act didn’t just change how R&D is treated going forward—it created a one-time opportunity to revisit the past.

Businesses that were required to capitalize R&D expenses from 2022 through 2024 now have a limited window to amend prior returns and recover those deductions.

That window closes on July 6, 2026.

What changed—and why timing now matters

For the past few years, Section 174 has created a disconnect for many businesses—especially in software and product-driven companies.

R&D costs that were once immediately deductible had to be capitalized and spread over multiple years. The results: higher taxable income, reduced near-term cash benefit, and confusion around how to plan to go forward.

With the new law, domestic R&D expenses are back. More importantly, there’s now a retroactive pathway to revisit those earlier years.

But this isn’t automatic. It requires a deliberate decision to amend prior returns—and that decision sits inside a fixed timeline.

For more details, read the latest blog about Big Changes to IRS R&D Tax Credit: What the New Form 6765 Means for 2024-25

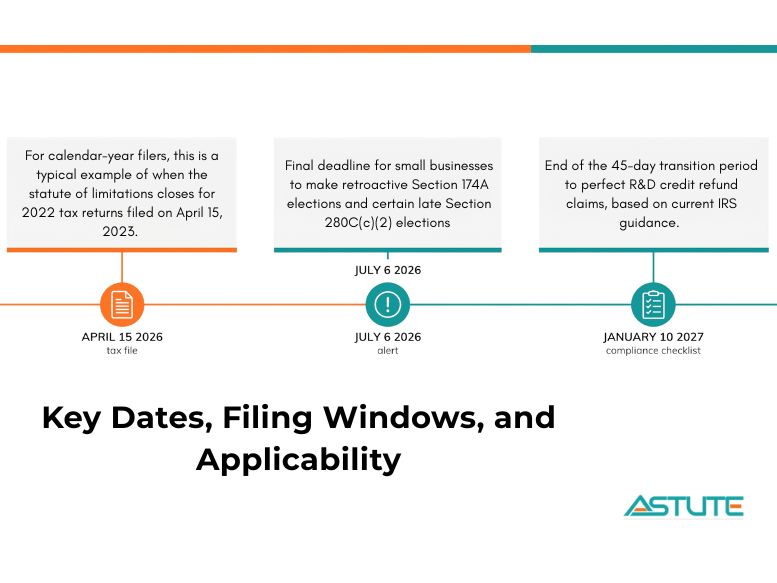

Key Dates, Filing Windows, and Applicability

| Date / Period | What It Means |

| April 15, 2026 | For calendar-year filers, this is a typical example of when the statute of limitations closes for 2022 tax returns filed on April 15, 2023. Your actual deadline may vary based on your original filing date. |

| July 6, 2026 | Final deadline for small businesses to make retroactive Section 174A elections and certain late Section 280C(c)(2) elections or revocations under Rev. Proc. 2025-28—unless your Section 6511 deadline occurs earlier. |

| January 10, 2027 | End of the 45-day transition period to perfect R&D credit refund claims, based on current IRS guidance. |

| Tax Year 2025 | Form 6765, Section G reporting remains optional for all filers. |

| Tax Year 2026 and beyond | Form 6765, Section G reporting becomes mandatory for most filers, with limited exceptions as outlined by the IRS. |

Important:

All deadlines are governed by the applicable statute of limitations. Under Rev. Proc. 2025-28, the effective filing deadline is the earlier of July 6, 2026, or the applicable deadline under Section 6511 for that specific tax year.

Why most companies will miss this

Most companies do not miss out because they don’t qualify. It’s because they haven’t decided.

What we’re seeing consistently:

- R&D credits evaluated in isolation, without considering Section 174

- No modeling of cash impact before amending returns

- Engineering work happening daily—but not translated into defensible claims

- Decisions pushed quarter after quarter until the window narrows

The underlying issue is not technical complexity—it’s lack of structured evaluation.

By the time the decision becomes urgent, the flexibility to act is already limited.

Read about Section 174 After OBBBA: R&D Expensing Rules for 2026 to know more about OBBBA Rule

Action Steps to Navigate OBBBA Requirements

- Confirm eligibility

Determine whether your business qualifies for retroactive relief under the One Big Beautiful Bill Act based on size, structure, and prior filings.

- Evaluate your 2024 R&E treatment

Review how research and experimental (R&E) expenses were handled in 2024—specifically, whether expensing was applied or capitalization was maintained.

- Assess amendment requirements

Identify which tax years (2022–2024) may need to be amended, particularly if expensing was not elected in prior filings.

- Prepare and align filings

Work with your advisor to prepare amended returns that are consistent across federal and state positions and supported by clear documentation.

- Execute within the deadline window

Submit all amendments by July 6, 2026, or earlier if your statute of limitations closes sooner.

This is a time-bound opportunity, and the window to act is limited.

Where Astute adds value

That requires more than eligibility analysis. It requires clarity on how the R&D credit interacts with Section 174, how it impacts cash flow, and whether the outcome holds up over time.

If you’re evaluating whether to amend prior returns, the real question isn’t just “How much can we claim?”—it’s “Does this improve our overall financial position?”

At Astute, we work with companies to evaluate that decision end-to-end. This includes assessing eligibility, modeling the financial impact of amending prior returns, and ensuring filings are aligned, well-supported, and defensible.

The goal isn’t just to claim credits. It’s to align the decision with cash flow, financial strategy, and long-term outcomes.

With the 2026 deadline approaching, the focus should be simple:

get clarity now, make the decision early, and avoid leaving value on the table.

Contact Us or Book a Free Call with Us