Introduction: Section 174 After OBBBA

For many businesses, Section 174 has been one of the most confusing and frustrating tax changes in recent years.

Starting in 2022, what was previously a simple deduction for R&D expenses became a capitalization and amortization requirement, frequently raising taxable income without enhancing cash flow.

With changes introduced under the One Big Beautiful Bill Act (OBBBA), the rules shifted again. While this brought relief for some taxpayers, it did not fully reset Section 174 to how it worked in the past.

In this blog, we will explain what Section 174 looks like now, how it impacts R&D and software development costs in 2026, and how businesses should think about planning going forward

Section 174 After OBBBA: Quick Summary

- Domestic R&D expenses may be deducted immediately in 2026.

- Foreign R&D expenses must still be amortized over 15 years.

- Software development is treated as R&E under Section 174.

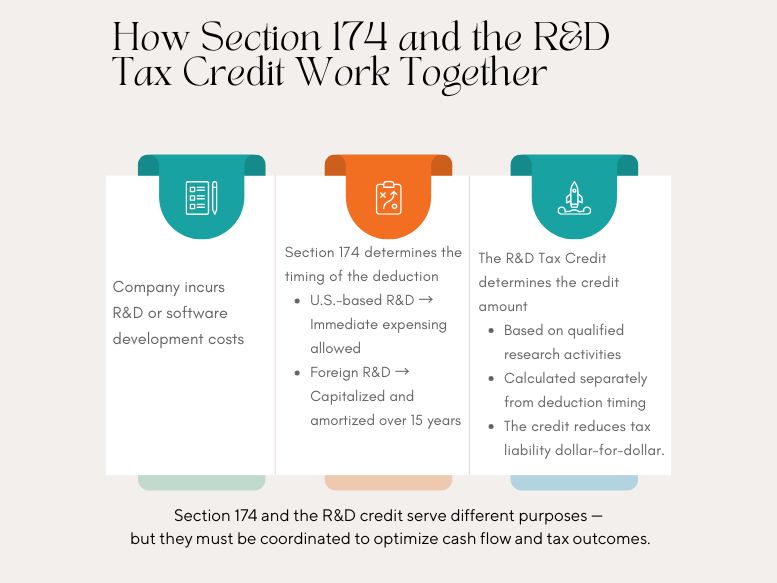

- Section 174 determines deduction timing; the R&D tax credit determines credit value.

- Strategic planning is required to optimize cash flow and compliance.

What Is Section 174?

Section 174 governs how businesses treat research and experimental (R&E) expenditures for tax purposes. These costs typically include:

- Product development and engineering

- Software development (including internal-use software)

- Prototyping and testing

- Process improvements intended to eliminate technical uncertainty

Importantly, Section 174 applies whether or not you claim the R&D tax credit. Many businesses learned this the hard way after 2022.

How Section 174 and the R&D Tax Credit Work Together

What Changed Under OBBBA?

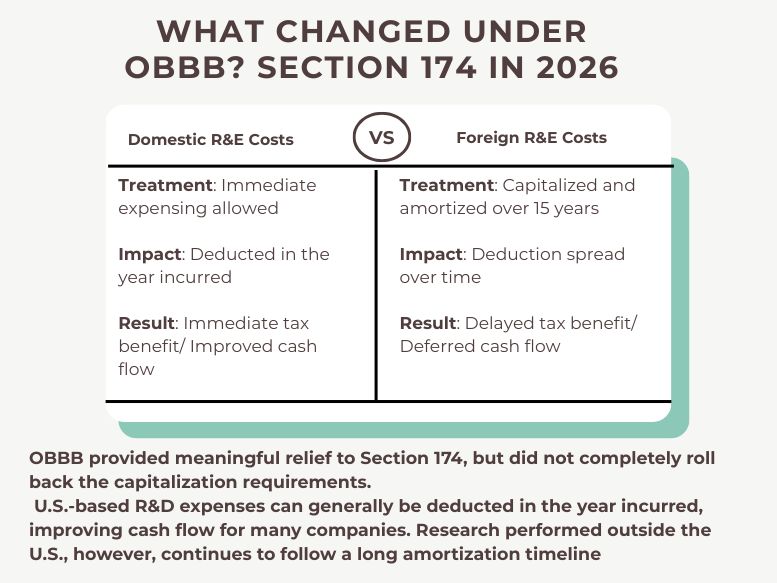

OBBBA provided meaningful relief to Section 174, but it did not completely roll back the capitalization requirements.

Here’s how the rules apply in practice for 2026.

| Type of R&D Expense | Current Tax Treatment |

| Domestic R&E costs | Immediate expensing allowed Deduct in year incurred—improves cash flow |

| Foreign R&E costs | Capitalized and amortized over 15 years Long amortization timeline—minimal near-term benefit |

| Software development (all types) | Treated as R&E under Section 174 Follows domestic or foreign rules based on where work is performed |

U.S.-based R&D expenses can generally be deducted in the year incurred, improving cash flow for many companies. Research performed outside the U.S., however, continues to follow a long amortization timeline.

What Changed Under OBBBA?

How Section 174 Works Now

Section 174 is no longer an “all or nothing” rule—it is largely location-based.

- If your R&D work is performed in the U.S., those costs may be deducted immediately.

- If the work is performed outside the U.S., the costs must still be spread over multiple years.

- Software development costs—whether customer-facing or internal—are explicitly included.

Tip: Many companies misclassify engineering or software costs as routine operating expenses. Under Section 174, proper classification matters more than ever.

How This Interacts With the R&D Tax Credit

A common misconception is that Section 174 replaces the R&D tax credit. It does not.

Here’s how they work together:

- Section 174 determines when R&D costs are deducted.

- The R&D tax credit determines how much credit is available for qualified activities.

- Coordination rules, such as Section 280C, still apply to prevent double benefits.

Businesses that track R&D properly can benefit from both immediate expensing and credits—if structured correctly.

Planning Opportunities for Tax Year 2026

This is where strategy matters more than compliance.

Key planning considerations include:

- Whether immediate expensing or optional amortization aligns better with projected income

- How previously capitalized costs should be handled

- Cash-flow implications for growth-stage or pre-profit companies

- Alignment between tax reporting and financial reporting

For some qualifying small businesses, retroactive relief may allow prior year returns to be amended. That said, amending is not always the right move—each option should be evaluated based on cash flow, future income, and overall tax strategy.

Practical insight: Section 174 decisions are most effective when made alongside forecasting—not after-tax returns are already prepared.

Common Section 174 Questions We Hear

Does this apply to startups?

Yes. Even early-stage companies with no revenue are subject to Section 174 rules.

Can prior returns be amended?

In some cases, yes—especially for qualifying small businesses—but eligibility and timing matter.

Do states follow these rules?

Not always. State conformity varies and can materially change the outcome.

What documentation is required?

Clear cost tracking, project descriptions, and consistent accounting treatment are essential.

What Businesses Should Do Next

If your company incurs R&D or software development costs, Section 174 should be part of your annual tax planning—not a year-end surprise.

Action steps to consider:

- Review how R&D and engineering costs are currently classified

- Separate domestic and foreign development activities

- Model expensing versus amortization outcomes

- Align R&D tracking with credit and deduction strategies

How Astute Helps Businesses Navigate Section 174

At Astute, we work closely with scaling businesses dealing with the real-world impact of Section 174—not just the theory.

Our work goes beyond compliance. We help clients:

- Properly identify and classify R&D Tax Credit and software development costs

- Separate domestic and foreign research activities to avoid overcapitalization

- Coordinate Section 174 deductions with R&D tax credits

- Model cash-flow and taxable-income outcomes before filing

- Prepare audit-ready documentation that aligns tax, accounting, and finance teams

Because Section 174 affects cash flow, forecasting, and long-term planning, we approach it as a strategic finance issue—not a last-minute tax adjustment.

Whether you are a startup building software, a scaling company investing in product development, or an established business refining internal processes, Section 174 planning should be intentional and forward-looking.